![[Credit: Adobe Stock]](https://www.kitplanes.com/wp-content/uploads/2026/03/AdobeStock_500023606_Editorial_Use_Only-1024x682.jpg)

Aircraft homebuilders face a unique and evolving insurance landscape that spans multiple phases—from initial kit purchase through construction, flight testing, and eventual operation. Unlike certified production aircraft with standardized risk profiles, experimental amateur-built (E-AB) aircraft present insurance underwriters with challenges rooted in variable workmanship, diverse designs, and limited fleet safety data. This report examines the essential insurance policies homebuilders typically need across the aircraft lifecycle, the liability considerations for pilots, and the regulatory framework that shapes coverage requirements.

The Three-Phase Insurance Framework

Choosing insurance for Homebuilt aircraft follows a distinctly different path from certified aircraft, requiring builders to navigate three sequential coverage phases that align with FAA certification milestones and operational restrictions.

Builder’s Risk Insurance: The Construction Phase

Before an experimental aircraft ever leaves the ground, it faces material risks in the workshop or hangar. Builder’s risk insurance—also known as project insurance or “ground not in motion” coverage—protects the accumulating value of components, materials, and labor during construction. This specialized coverage addresses perils including fire, theft, vandalism, weather damage, and damage during component transit.

A critical misconception among builders is that homeowner’s insurance policies will cover aircraft components within the home shop workplace. Standard homeowner’s policies rarely extend to aviation-specific materials, particularly once components are recognizable as aircraft parts. If a builder stores raw materials like sheets of aluminum or wood before assembly, homeowner’s coverage might apply, but once those materials take the form of wings, fuselages, or control surfaces, exclusions typically apply.

Builder’s risk policies are priced based on the documented value of the project at any given time. Carriers require builders to maintain detailed records—receipts for kit purchases, invoices for engines and avionics, and photographic documentation of construction progress. In the event of a loss, these records become the foundation for establishing claim value. Some policies include reimbursement for builder labor based on factory-estimated build times and reasonable hourly wages, though this is less common than pure materials coverage.

Importantly, builder’s risk insurance provides no coverage once the aircraft begins moving under its own power. The moment a builder starts taxi tests or conducts the first engine run-up with intent to move the aircraft, a transition to aircraft insurance becomes necessary.

The Experimental Aircraft Association (EAA) offers project insurance programs specifically designed for members building or restoring aircraft, providing both hull coverage for components and optional liability coverage for the construction workspace. Aviation Insurance Resources (AIR), BWI Aviation Insurance, and other specialty aviation insurers also offer project insurance with flexible terms tailored to the builder’s timeline—some kits remain under construction for years, while factory-assist programs may complete in months. Flight Coverage: Transitioning to Airworthiness

Once the FAA issues a special airworthiness certificate and the aircraft is ready for its maiden flight, builders must transition from project insurance to full aircraft insurance that includes both hull coverage (physical damage to the aircraft) and liability coverage (third-party bodily injury and property damage). This transition coincides with one of the most statistically dangerous periods in an aircraft’s life: Phase I flight testing.

Hull Coverage protects the aircraft itself against physical damage from virtually any cause—gear-up landings, loss of control, fire, hail, windstorms, collisions, and hangar accidents. Hull coverage is optional under FAA regulations, but lenders universally require it if the aircraft is financed, and most airports require it as a condition of hangar leases.

Aircraft hull policies are typically written on an “agreed value” basis, meaning the insurer and owner establish the aircraft’s value at policy inception. If the aircraft is declared a total loss, the owner receives the agreed value minus any applicable deductible, with no depreciation or market-value disputes. This contrasts with “actual cash value” policies common in auto insurance, where depreciation reduces the payout.

Coverage options for hull insurance include three tiers: ground not-in-motion (parked or stored), ground in-motion (taxi operations), and in-flight (all phases of flight). Most owner-operators select comprehensive coverage that protects the aircraft on the ground and in the air. Deductibles vary significantly by aircraft type and insurer practice. Many carriers writing light piston aircraft policies now offer zero-deductible hull coverage, while others impose set deductibles ranging from $500 to $2,500. For high-performance or complex experimental airplanes, deductibles may be structured as a percentage of hull value rather than a fixed amount.

Liability Coverage forms the financial safety net protecting builders and owners from third-party claims arising from aircraft operation. Standard liability policies provide coverage for bodily injury to persons not aboard the aircraft and property damage caused by the aircraft. The industry-standard limit is $1 million per occurrence for combined bodily injury and property damage, with a passenger sublimit of $100,000 per person.

Understanding liability policy structures is essential. Policies with per-passenger sub limits cap the amount paid per injured passenger regardless of the total occurrence limit. For example, a policy with $1 million occurrence limit and $100,000 passenger sublimit would pay no more than $100,000 per passenger even if four passengers were seriously injured in an accident—total passenger payouts could not exceed $400,000, leaving $600,000 available for third-party ground claims. “Smooth” liability coverage eliminates the per-passenger sublimit, providing the full occurrence limit available to all claimants on a first-come basis. Smooth coverage costs more but offers superior protection, particularly for aircraft with multiple seats.

Liability limits can be increased beyond the standard $1 million, with options typically including $2 million, $5 million, or higher, though securing limits above $1 million for experimental aircraft can be challenging due to the elevated risk profile underwriters assign to homebuilts. Commercial operators, charter services, and business aircraft commonly carry $5 million to $25 million in liability coverage.

Legal defense costs are included in most liability policies and do not erode the policy limit—meaning the insurer pays for attorneys, expert witnesses, and court costs separately from the occurrence limit itself. This represents significant value, as aviation litigation routinely generates six-figure legal expenses even when the insured party is ultimately found not liable.

Phase I Flight Testing: The Highest-Risk Period

The FAA mandates a Phase I flight testing period for all newly constructed experimental aircraft—typically 25 to 40 hours of flight time within a restricted geographic test area. During this period, the builder must systematically evaluate the aircraft’s performance, handling characteristics, and systems operation. Statistical data from the National Transportation Safety Board (NTSB) reveals that the first 50 hours of flight on a newly constructed E-AB aircraft are particularly hazardous, with 13 percent of all homebuilt accidents occurring during this fly-off period, most within the first 10 hours.

Insurance coverage during Phase I testing varies significantly by carrier and presents one of the most complex aspects of experimental aircraft insurance. Some underwriters provide liability-only coverage until Phase I testing is complete, suspending hull coverage entirely during the restriction period. Others offer hull coverage but with substantially higher deductibles—commonly 10 percent of the agreed hull value while the aircraft is “in motion”. For an aircraft valued at $100,000, this means a $10,000 deductible during Phase I, compared to perhaps $1,000 or zero deductible after Phase I completion.

Liability limits may also be reduced during Phase I, with some carriers offering only $500,000 in occurrence coverage during testing and prohibiting passenger coverage altogether. This reflects the practical reality that Phase I testing should not involve passengers—the FAA restricts Phase I operations to “crew” only, i.e., just the pilot.

Certain underwriters specialize in experimental aircraft and offer policies that include Phase I protection with full hull coverage from the first takeoff, though often with named-pilot restrictions, mentor-pilot requirements, and mandated test area compliance. Builders with extensive flight experience in the same type they’ve built, documented transition training, and detailed test plans have better access to comprehensive Phase I coverage.

The FAA’s Advisory Circular 90-116 introduced the Additional Pilot Program (APP), which allows homebuilders to have a qualified additional pilot on board to assist with flight tests, improving safety during this critical period. Some insurers favorably view participation in such programs when underwriting Phase I coverage.

Supplemental Coverages: Beyond Hull and Liability

Comprehensive aircraft insurance packages include or offer several additional coverages that address specific risks homebuilders face.

Medical Payments Coverage provides immediate payment for medical expenses when occupants are injured in the aircraft, regardless of fault. Typical limits range from $1,000 to $10,000 per person, including the pilot. This coverage serves a similar function to medical payments in auto insurance—enabling quick payment of emergency room bills, ambulance costs, or minor medical treatment without the delay and complexity of establishing legal liability. If liability is subsequently determined, the bodily injury portion of the liability policy would respond for additional damages beyond medical payments.

Search and Rescue Coverage reimburses costs incurred for emergency search and rescue operations following an accident or forced landing in remote areas. Standard limits of $25,000 cover helicopter rescue services, emergency medical evacuation, and related expenses.

Personal Effects Coverage protects passengers’ belongings—luggage, electronics, cameras, and other personal property damaged or destroyed in an aircraft accident. Typical limits range from $5,000 to $10,000 total, with per-passenger sub limits.

Emergency Off-Airport Recovery covers expenses associated with recovering an aircraft after an emergency or precautionary landing that did not result in damage—for example, a precautionary landing in a field due to weather, followed by professional disassembly and road transport back to the home airport. This differs from hull coverage, which applies only when the aircraft is damaged.

Hangar and Premises Liability extends coverage to accidents occurring in or around the hangar where the aircraft is based, protecting the owner from liability for injuries to visitors, contractors, or other persons on the premises. Limits typically range from $50,000 to $100,000.

Spare Engines and Parts Coverage protects the value of spare engines, propellers, and major components stored separately from the aircraft. For builders who purchase engines or quick build kits before completing their projects, this coverage bridges the gap between builder’s risk and aircraft insurance.

Cost Factors and Premium Determinants

Experimental aircraft insurance premiums vary dramatically based on a complex matrix of aircraft characteristics, pilot qualifications, operational factors, and market conditions. Understanding these variables enables builders to make informed decisions that can reduce insurance costs while maintaining adequate protection.Aircraft-Related Factors

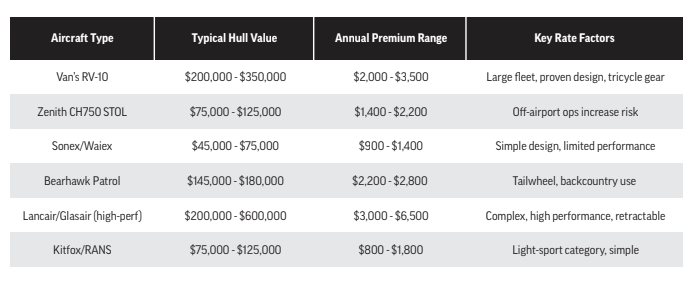

Aircraft Type and design pedigree ranks among the most influential premium determinants. Insurance underwriters favor well-proven designs with substantial fleet populations and predictable handling characteristics. Van’s Aircraft RV series enjoys particularly favorable treatment from underwriters due to the large fleet size (over 10,000 flying RVs), excellent safety record, conventional construction methods, and benign handling qualities. A builder completing an RV-10 can expect insurance quotes significantly lower than a builder completing a one-off design or a kit with a small fleet and limited safety history.

Hull Value directly impacts premium costs. Most insurers price hull coverage at approximately 1.0 to 1.5 percent of agreed hull value annually for piston experimental aircraft, with turbine and turboprop aircraft commanding slightly lower percentages (0.6 to 1.2 percent) due to different risk profiles. An RV-10 valued at $200,000 might carry an annual premium around $2,050, while a Zenith CH750 STOL valued at $75,000 might cost $1,650 annually.

Landing Gear Configuration substantially affects underwriting decisions and premium costs. Fixed tricycle gear aircraft receive the most favorable rates and lowest pilot experience requirements. Conventional gear aircraft demand higher pilot qualifications—typically a minimum number of dual instruction hours in type—and carry higher premiums due to increased ground loop risk. Retractable landing gear compounds complexity, particularly for low-time pilots, as gear-up landings represent one of the most common hull damage claims. Likewise, powerplant type influences both insurability and premium. For example, certified engines from Lycoming, Continental, or Rotax generally receive better treatment than automotive engine conversions. While many auto-engine conversions have proven reliable, underwriters view them as introducing additional mechanical uncertainty and parts availability concerns, leading to higher premiums or coverage restrictions.

Construction Materials and Methods factor into risk assessment. All-metal construction using established techniques receives standard treatment, while composite construction, moldless composite techniques, or unconventional structural approaches may face additional underwriting scrutiny.

Pilot-Related Factors

Total Flight Time and Experience in Type constitute perhaps the most significant premium variables under the pilot’s control. A pilot with 1,000 total hours and 250 hours in a Van’s RV-10 will receive substantially better rates than a pilot with 300 total hours and zero time in type building the same aircraft. The difference can approach 90 percent between highly experienced and minimally qualified pilots.

Transition Training demonstrates to underwriters that the pilot has received professional instruction specific to the aircraft type or category being insured. Completion of a recognized transition training program—such as Synergy Air’s RV transition course or a factory-sponsored training program for Glasair or Van’s—often results in premium reductions and improved coverage terms. Some insurers mandate transition training as a policy condition for complex or high-performance homebuilts.

Pilot Certifications and Ratings affect both insurability and cost. Instrument-rated pilots typically receive better rates than VFR-only pilots, as instrument training correlates with discipline, proficiency, and lower accident rates. Commercial certificates and ATP ratings further improve underwriting profiles. Pilot Age introduces complexity. While experience generally reduces premiums, advanced age can trigger rate increases. Pilots aged 65 and older may face significant premium increases, and some carriers impose age-based restrictions or decline coverage for pilots above certain ages, though practices vary by market conditions.

Claims History follows predictable patterns—a clean claims history over multiple years keeps premiums low, while a recent claim can increase premiums 10 to 25 percent for several renewal cycles.

Operational and Environmental Factors

Storage Method significantly impacts hull coverage costs. Aircraft stored in enclosed hangars receive premium discounts of 15 to 30 percent compared to aircraft tied down outdoors, as hangar storage protects against weather damage, hail, wind, and vandalism.

Base Location affects risk assessment. Operating from airports in regions prone to severe weather—tornado areas, hurricane-prone coastal regions, or locations with frequent hailstorms—increases premiums. Remember—it’s all about risk assessment. Remote locations far from maintenance facilities, such as in Alaska, may also cause higher costs. Conversely, basing at controlled airports with good weather and established maintenance infrastructure may reduce premiums.

Build Quality and Documentation directly influence underwriting decisions for experimental aircraft. Builders who maintain comprehensive build logs with photographs, records, weight-and-balance calculations, and adherence to manufacturer instructions receive favorable consideration. Factory-assist builds or builder-assist programs where significant portions of construction occur under professional supervision at the manufacturer’s facility net better rates than completely owner-built projects.

Regulatory Requirements and Mandated Insurance

A common misconception holds that aircraft insurance is federally mandated. In fact, the FAA does not require private general aviation aircraft owners to carry insurance. Unlike automobile insurance, which states universally require for road use, aviation insurance remains largely voluntary at the federal level for recreational and personal business use. For Part 91 operations—the regulation governing most private and business aircraft operations—no insurance mandate exists. An aircraft owner can legally fly an uninsured aircraft under FAA regulations, assuming full personal financial responsibility for any damage or injury caused.

State-Level Insurance Mandates

Aviation insurance requirements are primarily determined at the state level, with significant variation across jurisdictions. As of 2015, only 11 states had some form of liability insurance requirement or financial responsibility requirement for general aviation aircraft.

Minnesota stands alone in requiring nearly all GA aircraft owners to maintain liability insurance policies, with minimum limits of $100,000 per passenger seat. Other states with various forms of insurance or financial responsibility requirements include California, Florida, Oregon, and Virginia.

Most states—including Texas, Arizona, New York, Alaska, and Colorado—impose no liability insurance requirements for privately operated general aviation aircraft. However, the absence of state mandates does not mean aircraft owners in these jurisdictions operate uninsured. However, market forces, contractual requirements, and risk management prudence drive insurance purchases even absent legal mandates.

![[Credit: Adobe Stock]](https://www.kitplanes.com/wp-content/uploads/2026/03/AdobeStock_1545204580-1024x682.jpg)

Airport and Hangar Lease Requirements

Even in states without insurance mandates, aircraft owners routinely encounter insurance requirements through contractual relationships with airports and Fixed Base Operators. Most publicly owned airports require based aircraft to carry minimum liability coverage and name the airport authority as an additional insured on the policy.

Typical airport insurance requirements include:

• Liability Coverage: Minimum $1 million per occurrence for bodily injury and property damage.

• Additional Insured Endorsement: Airport authority, municipality, or FBO named as additional insured.

• Proof of Insurance: Current certificate of insurance on file with airport management.

• Primary and Non-Contributory Language: The aircraft owner’s insurance must be primary, with the airport’s insurance excess.

Hangar leases frequently impose additional requirements beyond basic aircraft liability. El Dorado County, California, for example, requires hangar lessees to provide aircraft liability insurance of $1 million per occurrence plus premises liability coverage. If the lessee sublets or rents the hangar to other aircraft owners, Hangar Keeper’s liability coverage of at least $75,000 or the value of stored aircraft becomes mandatory.

These contractual requirements create de facto insurance mandates for most aircraft owners, as basing an aircraft at a public airport or renting hangar space without insurance becomes impractical.

Lender Requirements

Aircraft owners who finance their purchases face the most stringent insurance requirements of all. Banks, credit unions, and specialized aircraft lenders universally require comprehensive insurance as a condition of financing.

Typical lender insurance requirements include:

• Hull Coverage for full replacement value or loan amount, whichever is higher; Breach of Warranty Clause that protects the lender even if the pilot violates policy terms.

• Loss Payee Endorsement: Ensures lender receives proceeds in case of total loss.

• Minimum Liability Coverage: Typically, $1 million per occurrence.

Lenders require continuous proof of insurance throughout the loan term, and any lapse in coverage typically constitutes a loan default, potentially triggering acceleration of the full loan balance.

Next time, we’ll examine the homebuilder as manufacturer and the issue of product liability insurance

![[Credit: EAA]](https://www.kitplanes.com/wp-content/uploads/2026/03/aerial-2025-looking-sse-lowres-by-connor-madison_350_350.jpg.jpeg?w=324&h=160&crop=1 "The Rites of Spring")

The assertion that upon receiving an airworthiness inspection, “builders must transition from project insurance to full aircraft insurance that includes both hull coverage (physical damage to the aircraft) and liability coverage (third-party bodily injury and property damage)” is incorrect and contradicts statements elsewhere in the article. Many owner/builder pilots, since they built the plane and they would be the ones doing repairs anyway, simply fly with liability insurance and no in-motion hull coverage.

Perhaps I should have used the word “should” in place of “must” but flying under-insured is a fine way to lose a big investment in airplane, work, and time.

Comments are closed.